As of 1st July 2018, a Federal Government plan aimed at sealing a multi-million-dollar revenue hole will make buying new property more complicated.

When a developer sells a new property, the price includes GST, so the developer must pay 1/11 to the Australian Tax Office with its next Business Activity Statement.

However, some smarty-pants investors figured that they could take the whole amount paid by the property buyer to pay out the bank and the trade creditors, including a fat “management fee” to entities associated with the developer. Then, oh dear, no money left to pay the GST, so nothing for it but to tip the development company into liquidation – leaving one major unpaid creditor, the ATO.

As financial engineering goes this is definitely low-tech, so we may wonder why it has taken so long to do something about it. Finally, something is being done.

From the 1st of July 2018, the Government is transferring the responsibility of GST payment to the property purchaser. Moving forward, buyers of new residential premises or potential residential land will be required to withhold an amount from the price and pay this amount to the ATO on or before settlement.

This change will apply to any contract entered into before 1 July 2018 where settlement occurs after 1 July 2020 (even if the settlement date was originally set for a date earlier than this) and to all contracts signed after 1stJuly 2018.

It does not include: second-hand property, non-residential property, commercial residential property (such as hotels, boarding houses) or new residential property through substantial renovation.

How will the new GST payment rules work?

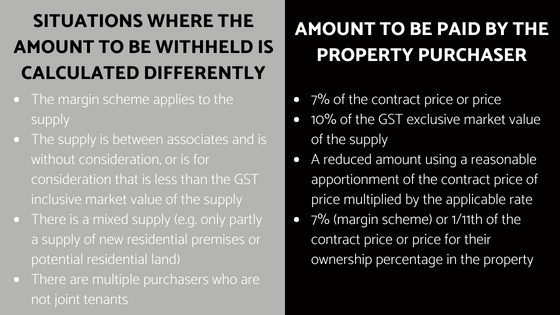

Generally, if the property sale contract specifies an amount that is the price of the supply (e.g. the contract price), then the withholding amount for the GST obligation is calculated on the contract price.

However, there are some situations in which the amount to be withheld is calculated differently, as outlined in the table below:

To assist property purchasers with these new arrangements, the property vendor must notify the buyer in writing of their GST withholding obligations and inform them of how much it is and when it is due to the ATO.

What are the legal impacts of these new changes?

The changes to the GST payment on new properties has numerous legal implications for both property vendors and buyers:

Property purchasers

Buyers need to be aware of their GST payment requirement and should seek legal advice to ensure that the GST gets paid correctly and on time or they risk facing penalties from the ATO if the funds are not remitted correctly. Other considerations may include incurring additional compliance or conveyancing costs in the property purchase process.

Property developers

There are also several legal impacts that property developers will need to consider moving forward. Not only will they need to review and amend their settlement statements and procedures to ensure compliance with the new changes, but they will also need to consider the potential cash flow consequences, as they will no longer benefit from the GST component of the sale proceeds in their bank account for the period between settlement and lodgment of their Business Activity Statements (BAS).

Whilst this one big change to how GST is paid will close down a significant tax evasion opportunity, it will simultaneously result in many different actions and outcomes for both property developers and purchasers. Both parties need to be aware and across the new obligations in order to avoid any financial or legal fallout of non-compliance.

If you would like to know more or need any assistance, feel free to contact us at Antcliffe Scott, we’d be more than happy to help!